About

About

Online

Online

Data

Data

The unbanked people of the world are so much more than a population in need of help. They’re a potential customer base waiting to enter the formal economy—and push it to new heights.

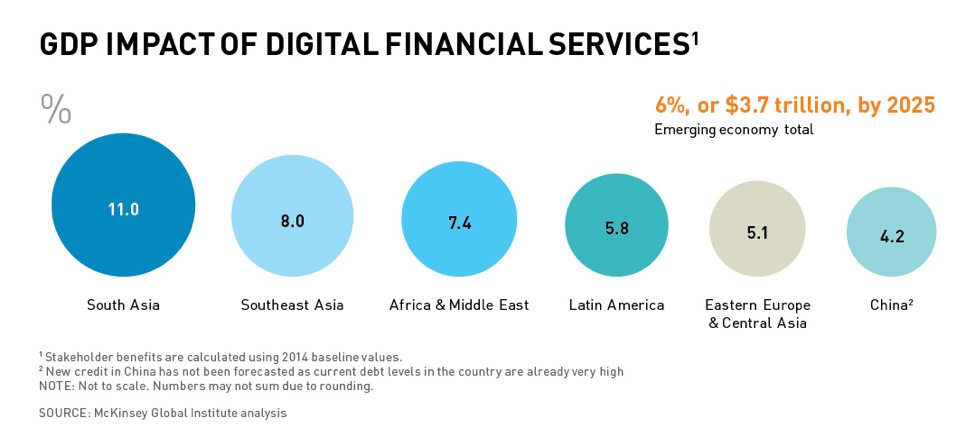

A new report recently released by the McKinsey Global Institute demonstrates how digital financial services (DFS) can drive financial inclusion and economic growth at the same time.

According to Digital Finance for All: Powering Inclusive Growth in Emerging Economies, DFS can:

There are significant gains for financial services providers as well. DFS would save providers $400 billion by making processes more efficient. And by taking on more than a billion new customers through digital accounts, providers would add more than $4.2 trillion to their balance sheets.

The report, which I was honored to contribute to, makes use of MGI’s proprietary GDP growth model, combined with inputs from 150 expert interviews representing seven large emerging countries. And it comes at a time when interest in financial inclusion is reaching a new peak.

Last year, the UN highlighted financial inclusion as a way to drive progress toward the 17 Sustainable Development Goals. And just recently, the G20 drafted eight High-Level Principles for Digital Financial Inclusion, providing a basis for how countries can use digital technology to create a more inclusive economy. The MGI report validates the global commitment to DFS and adds to the momentum making digital financial inclusion a very real and attainable prospect.

I shared early findings from the report at AFI’s Global Policy Forum in early September. It sparked some great discussion, but the thing I remember most clearly was the feeling in the room. AFI’s membership is passionate to begin with, and the way this report validated one of their central ambitions—getting more digital financial products into the hands of more people—ignited their resolve like I’d never seen.

Now we have to carry that excitement into all the conversations and collaborations we’ll have as we work toward achieving digital finance for all. According to the report, we should focus our work on three main pillars: building out the digital infrastructure, fostering a dynamic and diverse market, and filling that market with the right set of products.

In terms of infrastructure, we need to continue the expansion of mobile and internet coverage in developing countries. We need to explore digital IDs, which are an increasingly affordable way to help unbanked people sign up for accounts. And we need balanced regulation of telcos and payment providers, to mitigate the advantages and disadvantages of potential providers and give each one a fair shot when entering the market.

In terms of dynamism and diversity in the market, we need to balance the protection of customers with the promotion of innovation. Privacy and security of personal accounts are always paramount, and never more so then when reaching out to customers who may be slow to trust a digital alternative to cash. At the same time, a young industry like this depends on multiple providers moving quickly and competing with each other. We need regulations that inspire, rather than stifle, that kind of commerce. Risk-proportionate regulation in lower-value products, such as regulatory sandboxes and tiered know-your-customer requirements, are ways of striking the balance we need.

And in terms of products, generally we need low-fee and easy-to-access options like mobile money. But there are more specific needs we don’t yet understand fully—what kinds of features would benefit a smallholder farmer? What about a female head of household? There are nuanced needs within and throughout the unbanked population. And just as there are endless financial instruments catering to the disparate needs among the middle and upper class, we need to develop products to accommodate specific needs and lifestyles within the unbanked population.

AFI, with its focus on knowledge sharing, will be a vital agent in pursuing these goals. Because nothing above can be achieved by any one committee, agency, government, company, or sector. We all have a role to play.

The new McKinsey report gives us even more incentive to continue the work we’ve been championing for years. And it gives anyone out there who is ambivalent about financial inclusion something to think about. Maybe they’ve heard that DFS can help bring the unbanked into the formal economy. But did they know it can create a $3.7 trillion bump in GDP?

It can. So now we know, without a doubt, that everyone benefits from an economy that includes everyone.

ABOUT THE AUTHOR

Jason Lamb is the Deputy Director of Financial Services for the Poor at the Bill & Melinda Gates Foundation.

© Alliance for Financial Inclusion 2009-2024