About

About

Online

Online

Data

Data

By Ghiyazuddin Mohammad, Senior Policy Manager, Digital Financial Services and Adeyemi Omotoso, Policy Specialist, FinTech, AFI

Buoyed by ongoing physical distancing and mobility restrictions, BigTech firms and digital platforms have become one-stop shops that are helping mitigate the negative effects of the COVID-19 crisis by meeting users’ financial and non-financial needs. By acting as virtual marketplaces, digital platforms are providing individuals and small businesses with access to information, markets and financial services, while also helping remotely onboard customers and offering products and services in a safe and secure manner.

Contrasting the 2008 global financial crisis, when regulators and financial supervisors provided bail outs to corporations considered “too big to fail”, a bottom-up approach of working with vulnerable groups, such as MSMEs, women and elderly, is needed this time to accelerate recovery.

In response, AFI organized a webinar on 14 May 2020 for regulators and digital platforms, including China’s Alipay and Nigeria’s Jumia, to gain a deeper understanding of how BigTechs and digital platforms can respond to the human and economic impact of the global pandemic and devise appropriate regulatory interventions. Three key elements emerged as over 190 AFI members and partners discussed a range of topics, and in combination with additional analysis.

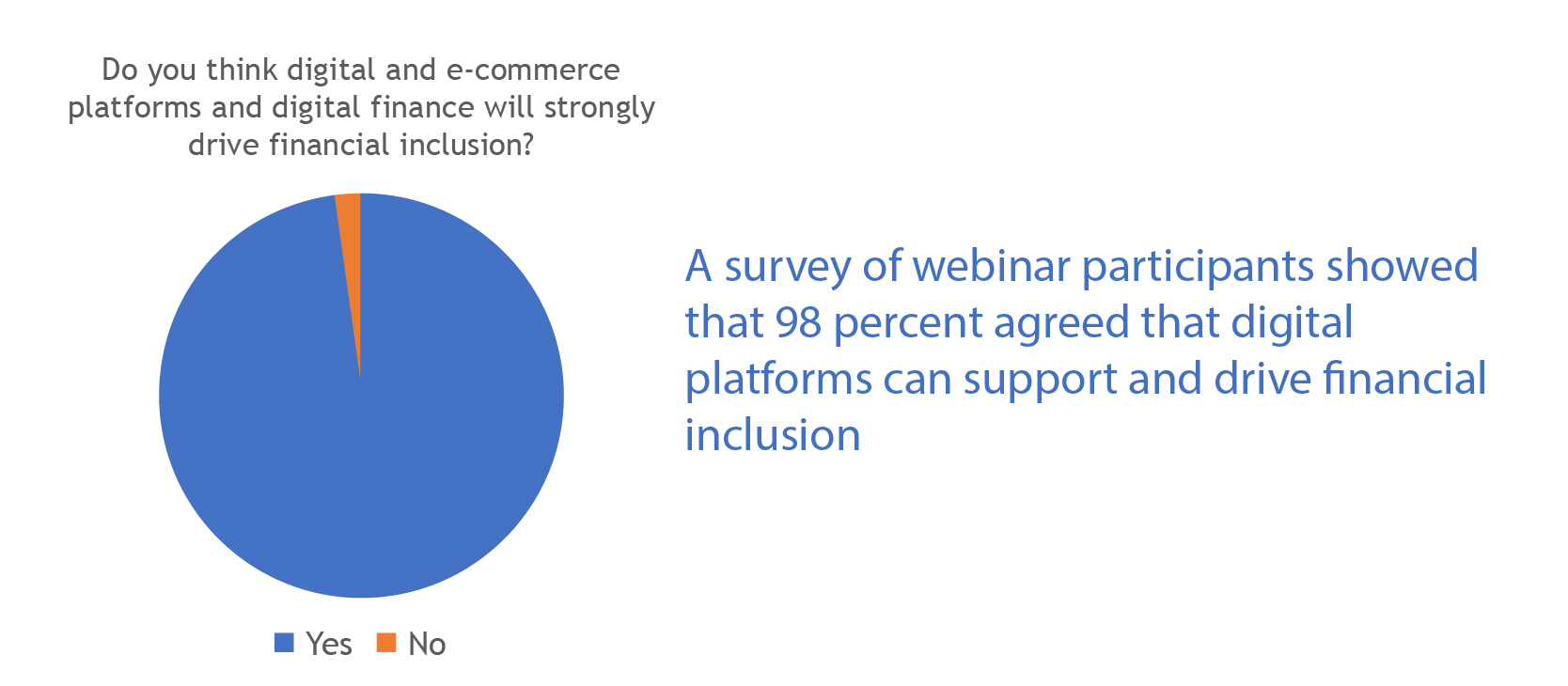

1. Innovative approaches deepen financial inclusion

![]()

Digital platforms provide essential services that enable the supply and delivery of basic groceries to support small businesses (such as restaurants and online retailers), facilitate the payment of government aid and enable digital financial services (such as payments, credit and insurance). Some notable examples include:

Alipay: Supported small businesses and vulnerable segments by reducing or waiving platform fees and providing low-interest and interest-free loans, personnel and logistics support for the delivery of essential goods and services. In collaboration with the Reliable Medicine-Sourcing initiative, Alipay, under the Alibaba brand, worked to ensure that crucial prescription drugs could still reach about 300 million patients suffering from chronic illnesses across China. They onboarded almost 50,000 offline micro, small and medium enterprises (MSMEs) and issued digital coupons in more than 100 cities to encourage consumer spending.

Grab, a ride-hailing, food delivery and payment technology company, supported platform economy employees and small business partners in Malaysia by providing health and social cover of up to MYR1,000 (USD225) per driver affected by the pandemic and MYR300 (USD67) towards the purchase of essential food and grocery items. MSMEs were given up to MYR3,000 (USD674) in relief in the form of rebates on order surcharges and commission.

Jumia, an online marketplace for electronics, fashion, logistics and payment services in Africa, implemented contactless delivery for prepaid essential packages as part of measures to enhance the safety of customers and workers during the pandemic.

Gojek, a multi-service platform for ride-hailing and digital payments, offered financial aid to support its more than 1.7 million drivers in 167 cities and districts across Indonesia, and helped drive demand for its over 500,000 merchant partners – of which 96 percent are MSMEs – after they migrated online.

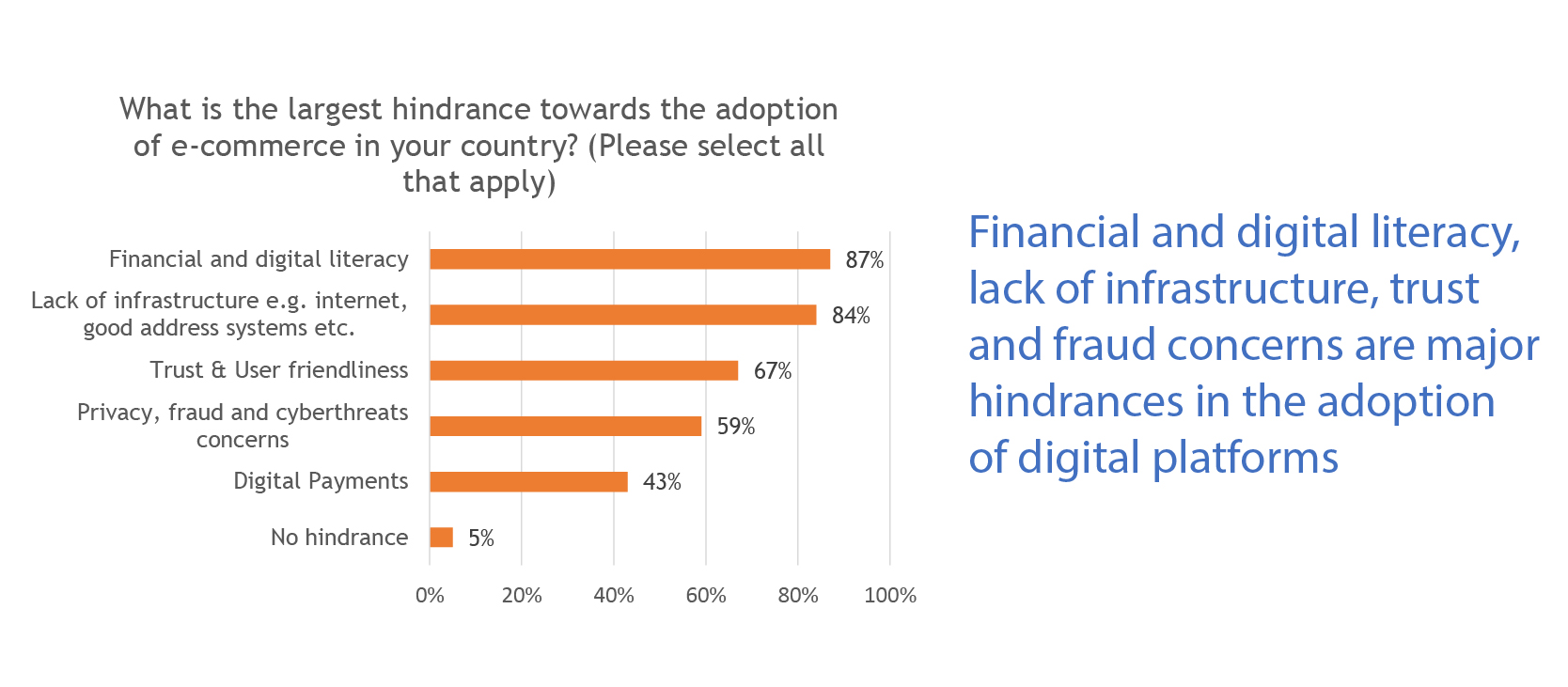

2. Opportunities to build and grow

![]()

While digital platforms may have the potential to play a critical role in the current crisis and beyond, regulators expressed concerns that low levels of financial and digital literacy threaten to curb adoption rates (see figure above). Limited access and usage of digital devices have made these concerns even more prominent among vulnerable segments, especially women, elderly and forcibly displaced.

A lack of adequate digital infrastructure, including reliable mobile networks and stable internet connections, also came out as major hindrance, particularly in emerging market economies. Other main obstacles related to user-friendliness, include privacy, fraud and cybersecurity continue to negatively affect trust in digital platforms.

3. Consensus on an enabling regulatory environment

Regulators and policymakers need to work with digital platforms and broader stakeholders to address any shortcomings in the financial capability, data privacy and security of these platforms, and help build trust and credibility. This additionally underscores the growing importance of policy, regulation and governance as digital platforms expand and become dominant in the daily lives of consumers.

Even so, authorities need to take a cautious and gradual approach in regulatory interventions. A good starting point is to foster public and private dialogue at the global and regional level, which can then feed into country-level discussions.

Given the nature of digital platforms, regulators also need to engage with domestic authorities involved in data protection, competition, information and communication technologies, and other relevant areas. Such discussions and engagements can further encourage “test and learn” approaches, including regulatory sandbox, innovations hubs and accelerators, giving players space to test financial products, services and delivery mechanisms.

However, controlled testing should not compromise financial literacy and consumer protection. Digital-first models must capitalize on various platforms and channels to enhance the financial capabilities of vulnerable populations in a behaviorally informed manner.

Furthermore, data protection and privacy are highly relevant given the greater use of data in the delivery of financial services. Authorities need to assure mutually beneficial relationships between customers and digital platforms to safeguard that the collection of consumer data does not exceed what is required, that it is done with consent and not sold to third parties for financial gain.

For women, who suffer the addition burden of a digital gender divide, the adoption and use of digital platforms and BigTech includes barriers to access, affordability, education (or lack thereof) as well as a lack of technological literacy. All these factors compound inherent biases and socio-cultural norms that lay the foundations of gender-based digital exclusion, and potentially translate into increased growth in digital payments and financial services that further exacerbate the gender gap.

Policymakers and regulators must respond immediately by collecting sex-disaggregated data to develop gender-sensitive policies. Looking ahead, stakeholders need to collectively address underlying issues of ownership and usage of digital devices as well as access to internet among women and other vulnerable segments.

The way forward

Some emerging and developing economies are reporting exponential uptake in digital transactions, including payments, online retail purchases and digital financial services. Reflecting changing behavior, as a result of the global pandemic stimulating digital and financial onboarding and sustained growth, we continue to encourage policymakers and financial regulators to seize these opportunities and use digital technologies to accelerate recovery, re-ignite commerce and deepen financial inclusion.

© Alliance for Financial Inclusion 2009-2024