About

About

Online

Online

Data

Data

12 March 2021

By Diana Schvarztein, Policy Manager, AFI

Today more than ever, young people are needed at the core of regulatory and policy interventions. These are the 1.2 billion people aged 15 to 24 years worldwide who are key to a demographic dividend, economic growth, political stability, innovation as well as social and sustainable development.[1]

Despite their huge potential, barriers from the regulatory, supply side and demand side leave nearly half of all young people excluded from formal financial services in developing economies. This generation also faces unprecedented hardship with multiple shocks linked to the fallout from COVID‑19, including disruptions to education and training, job losses, depleted income and increased difficulties in finding employment[2]. The ongoing economic crisis caused by COVID-19 has further amplified young people’s need for mechanisms to invest in income-generating activities and improve their financial resilience in the face of financial shocks.

This backdrop of uncertainly underscores the timely launch of AFI’s Youth Financial Inclusion Policy Framework – the network’s first knowledge product in this thematic area – with the aim of providing specific regulatory and public policy approaches to advance the youth financial inclusion agenda by drawing on the experiences of AFI members.

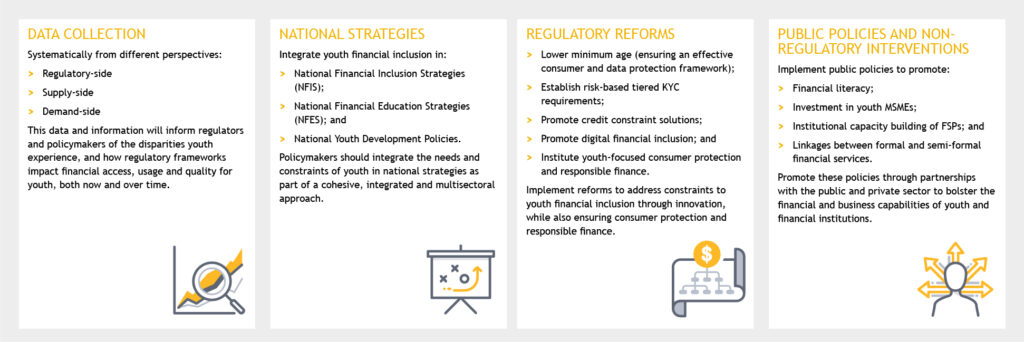

In the policy framework, AFI experts outline how the youth financial inclusion agenda can be advanced considering four pillars:

Systematically collecting and analyzing national data allows policymakers and regulators to develop a more precise understanding of the characteristics, financial needs and types of barriers youth face.

From the demand side, this means drilling down into young people’s financial access, usage and quality of financial services, disaggregated by age, gender as well as other context-appropriate variables. Meanwhile, the regulatory side looks at mapping financial inclusion policies and regulations tailored or applied to youth while the supply side identifies financial and non-financial services tailored to this segment.

In the Philippines, for example, efforts to collect national demand-side data led to the youth segment being embedded in financial inclusion surveys (FIS) conducted every two years by Bangko Sentral ng Pilipinas. FIS respondents are 15 years old and above with their data split into various age brackets such as 15–19 years, 20–29 years and 30–39 years.

Integrating youth needs and constraints into various national strategies and policies – including for financial inclusion and youth development – should follow cohesive and multisectoral approach. This allows focused, coordinated and integrated implementation of a national plan tailored to meet the needs of the youth.

Across the AFI network, 16 member institutions include youth either as a main target or cross-cutting group in their national financial inclusion strategies, including Central Bank of Jordan, Central Bank of Solomon Islands and Reserve Bank of Zimbabwe.

Although the financial inclusion of youth varies between countries, several common regulatory barriers exist, including age restrictions, Know Your Customer requirements and an absence of financial records, credit history, traditional collateral and guarantees.

Mexico’s response to the age restrictions saw the introduction of regulatory reforms that allowed 15-17 years old to open bank deposit accounts as of March 2020. According to the Comisión Nacional Bancaria y de Valores, these accounts could receive digital transfers from government scholarships or salaries from companies but also had limits on yearly deposits and were exempt from commissions. They could be opened in person or remotely and one representative of the young person must be notified of the opening of the account.

This development, however, highlights the need for greater consumer protection. With many young people using digital financial services for the first time, it is important to implement an effective consumer and data protection framework that reinforces trust in digital financial tools and encourage responsible use.

Implementing public policies enhances financial literacy, investment in youth micro, small and medium enterprises and the institutional capacity building of financial service providers. State Bank of Pakistan implemented the country’s first e-learning financial literacy course, which is delivered through an engaging and interactive game. Called PomPak – Learn to Earn, the game targets three age groups – children (9-12 years old), adolescents (13-17 years old) and youth (18-29 years old) – and can be accessed through a desktop browser or a dedicated mobile phone application.

Additional examples by AFI members are provided throughout the policy framework in each of the four dimensions as brief case studies as well as regulatory and policy recommendations. Gender-specific concerns are addressed in all sections as a cross-cutting theme.

As countries experience different challenges and opportunities in youth inclusion, the policy framework can be adapted to their specific national contexts, including those that address the heterogeneity and diversity of young people and their distinct life stages.

Through the policy framework, the AFI network encourages policymakers to position youth at the core of policies and regulations and ensure their access to effective financial tools. The sustainable livelihoods of the youth depend on their resilience to financial shocks from an early age.

AFI’s Youth Financial Inclusion Policy Framework can be found here.

[1] World Youth Report, 2018.

[2] International Labour Organization, 2020)

© Alliance for Financial Inclusion 2009-2024