Dr Peter Knaack, Research Associate, Centre for Sustainable Finance at SOAS, University of London; Adjunct Professor, School of International Service, American University; Associate, Council on Economic Policies

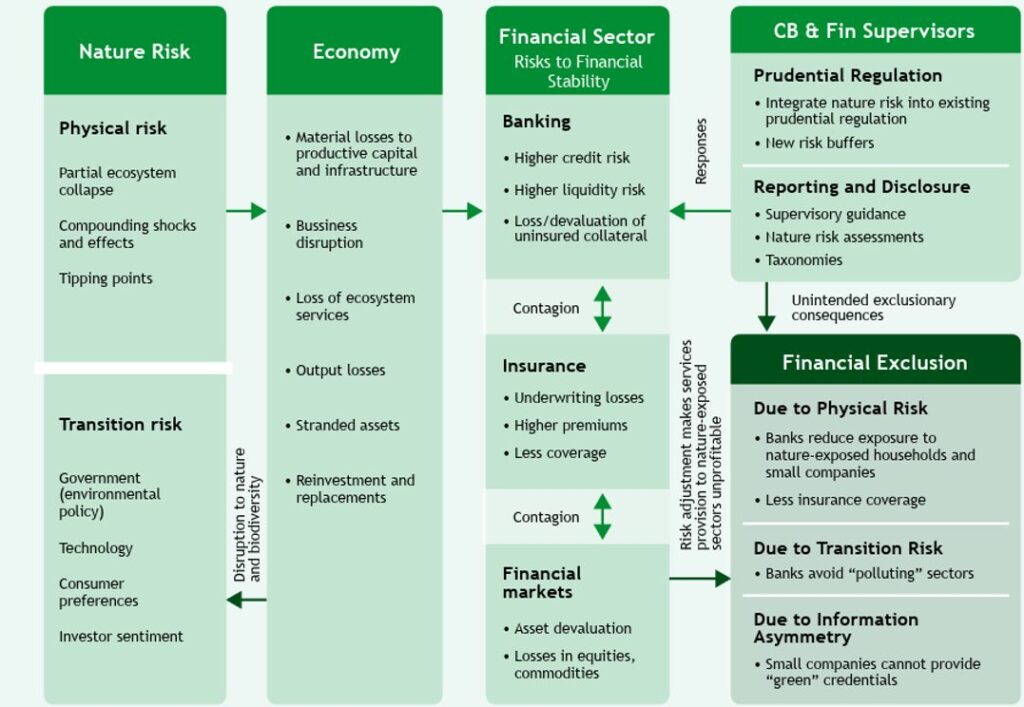

In a drought-hit rural district, a supervisor reviews rising non-performing loans in agricultural portfolios. At first glance, the problem looks familiar: weak collateral, volatile incomes, rising defaults. But the deeper cause sits outside the balance sheet. Soils are exhausted, pollinators have disappeared, water sources are unreliable, and productivity is falling year after year. What begins as nature loss ends as credit risk, insurance withdrawal, and financial exclusion.

This is the reality confronting a growing number of central banks and financial supervisors in developing economies today.

Embedding Biodiversity Considerations into Inclusive Green Finance Policies, a new AFI special report, makes the case that biodiversity loss is no longer a peripheral environmental issue, but a financial stability and inclusion challenge. More than half of global GDP depends on nature, yet global wildlife populations have declined by almost 70 percent since the 1970s, with over one million species at risk of extinction. These trends translate directly into higher physical and transition risks for financial institutions, especially in developing economies where agriculture, fisheries, and tourism dominate both employment and loan books.

Nature risk is becoming inclusion risk

The report shows how biodiversity loss and financial exclusion can reinforce each other. Nature degradation reduces incomes and raises volatility for smallholder farmers, fishers, and small companies. Financial institutions respond by repricing risk, tightening lending standards, or exiting entire sectors. The result is a vicious cycle in which those most dependent on ecosystem services face higher borrowing costs, less insurance coverage, or no access to finance at all.

The distributional implications are hard to ignore. Nearly 80 percent of people in low-income countries are exposed to multiple environmental stressors, compared to just 1 percent in high-income countries. Poor households are far more likely to live on degraded land. In countries like Zambia, more than three quarters of financial sector exposures depend on multiple ecosystem services, turning biodiversity loss into a system-wide vulnerability.

When prudential action backfires

The report also offers a cautionary note. Supervisory responses to nature risk are expanding fast. By 2025, financial authorities in 25 jurisdictions had begun integrating nature related risks into prudential frameworks. While necessary, these efforts can have unintended exclusionary effects if they are not carefully designed.

Stricter due diligence requirements, complex taxonomies, and costly certification schemes often exceed the capacity of small firms and smallholders. Sustainability certifications can cost ten thousand dollars or more. In the European Union, less than 2 percent of SME lending qualifies as green under the taxonomy. Evidence from Brazil shows that environmental risk regulation reduced lending to small firms in environmentally risky sectors by up to 3 percent, without delivering clear environmental benefits.

For supervisors with financial inclusion mandates, this creates a dilemma. Managing nature risk through blunt instruments can improve measured resilience while quietly pushing vulnerable clients out of the financial system.

From trade-offs to policy design

The report’s central contribution is to move the debate beyond trade-offs. It argues that central banks and supervisors can actively shape a virtuous cycle of nature-positive and inclusive finance, if policy design is proportional, data-driven, and grounded in local realities.

AFI distills this approach into four clear policy directions.

- Incorporate nature into public sector financial planning

- Create an enabling environment for nature-positive products and services

- Make data on nature and nature finance accessible

- Bolster demand-side drivers of sustainable production

First, biodiversity should be embedded into national financial inclusion strategies and inclusive green finance frameworks. This means aligning inclusion targets with nature-positive outcomes in sectors like agriculture, fisheries, and tourism, and working closely with public development banks to combine capacity building and finance for practices such as agroforestry and restorative agriculture.

Second, supervisors should create enabling environments for nature-positive financial products. Rather than relying solely on rigid taxonomies, authorities can support inclusive payment for ecosystem services schemes and community-based conservation finance such as blue recovery bonds, while using test-and-learn regulatory approaches to avoid excluding small actors.

Third, nature data must be made accessible and affordable. Georeferenced credit registries that use GPS and remote sensing data can dramatically lower the cost of assessing biodiversity risk and compliance, reducing information burdens on small borrowers while strengthening supervisory oversight.

Finally, demand-side drivers matter. Policies that connect small producers to higher-value markets and support community-focused financial services can improve both biodiversity outcomes and borrower creditworthiness over time. The report gathers examples from Mozambique’s Coastal Lifeline Project and China’s Taobao Villages to Brazil’s Living Amazon Mechanism to illustrate that community business can be both nature-positive and financially viable.

A supervisory agenda for the next decade

The message of the report is clear. Nature loss threatens to reshape risk profiles across financial systems, particularly in developing economies. Central banks and financial supervisors sit at a critical junction where environmental degradation, financial stability, and social inclusion meet. Their actions will help determine whether the transition produces a more resilient and inclusive financial system, or one that protects balance sheets at the expense of those most exposed.

AFI’s Inclusive Green Finance workstream is supported by Agence française de développement.

LEARN MORE: Embedding Biodiversity Considerations into Inclusive Green Finance Policies