About

About

Online

Online

Data

Data

By Luis José Arredondo Heredia, General Director of Supervision of Savings and Loan Cooperatives, CNBV

Responding to the growing economic uncertainties amid COVID-19 restrictions, Mexico’s Comisión Nacional Bancaria y de Valores (CNBV) recently launched a special accounting standard that allows financial intermediaries, such as banks, financial cooperatives, popular finance companies and credit unions, to support individuals and micro, small and medium enterprises (MSMEs) affected by the ongoing crisis.

Introduced in March 2020[1], the new facility was designed to ease some of the financial pressures facing MSMEs struggling to cope amid the closure of non-essential[2] economic activities. In addition to offering discounts, grace periods and revised payment schemes, it also provides additional liquidity during the ongoing period of restrictions. Through the facility, financial intermediaries – which hold 64 percent of business portfolios linked to non-essential activities – are encouraged to redirect credit to MSMEs through risk-sharing measures, such as public credit guarantees.

With large sections of Mexico’s economy temporarily closed since 31 March 2020 due to the ongoing pandemic, the financial viability of many MSMEs remains uncertain. Demonstrating the sheer scale of the downturn, industrial production fell by 29.6 percent year-on-year in April 2020, the biggest-ever recorded drop.

Amid an uncertain outlook, the new accounting facility benefits clients by ensuring that payment histories kept by borrowers at the credit agency are not affected by non-payments. It also provides the opportunity to extend payment terms by six months, or 18 months for agriculture, livestock, forestry, fishing, industrial, commercial and service sectors. This provision also includes loans intended to finance other activities in cities with up to 50,000 inhabitants.

Furthermore, contractual modifications must not include explicit or implicit additions in unpaid interest, while financial restructuring must not generate additional costs or commission. Regarding existing revolving credit lines, these must not be restricted or decreased by more than 50 percent of the part not disposed and no additional requested for guarantees or replacements will be made.

For financial intermediaries, they are also benefiting by being able to design refinancing solutions that better meet the needs of individuals and MSMEs reporting late payments after February or March 2020. Portfolios of MSMEs with outstanding payments from before this period, however, will not be affected by the standard.

In more detail, changes to mortgage-backed loans that cannot be updated before a legal notary will still be guaranteed, provided they are documented by a signed contract. This lower risk profile translates into lower costs linked for potential loan impairment charges and limited impact on capital adequacy.

Loans able to benefit from the new accounting facility include those that were restructured in the past, have periodic payments and reported arrears of 90 days or more. Loans must be classified as belonging to a current portfolio as of 28 February 2020 for banks, and as of 31 March 2020 non-bank intermediaries.

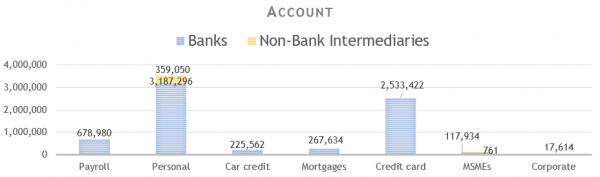

The facility has already proved popular, with financial intermediaries having restructured 3.6 million loans belonging to individual and MSMEs worth USD9.2 trillion as of end-May 2020.[3] This surge in data has allowed for the greater analysis of borrowers’ payment capacities and cash flows.

![]()

![]()

Despite this, CNBV does not plan to extend the measure. Given expectations of improvements in the economic outlook, the accounting facility will only be applicable for a set period. When normal activities resume, standards will be restored to ensure that a combination of vulnerabilities and looser regulation do not cause future crises.

Significant uptake of this facility has given rise to several disadvantages, not least the limited manpower linked to a high level of requests but fewer staff being available to carry them out, due to movement restrictions still in place. Financial intermediaries were given 120 days to restructure the operations of individuals and MSMEs that requested support. Furthermore, technical and administrative changes must be reflected in accounting and operating systems, while disclosure notes must be added to financial statements and monthly reports provided to CNBV.

This new facility is unique among AFI members, which have largely focused their efforts towards assisting MSMEs with mitigating and recovery measures such as fiscal packages, monetary structural policy and exchange rates and balance of payments. With this new facility, CNBV expects that it will ease the liquidity challenges that beneficiaries have faced due to the ongoing economic downturn. Even so, is it estimated that the protracted nature of the ongoing crisis will see three in every five cases suffer from non-payments. As such, regulators are urged to bolster their support for MSMEs and continually develop new and innovative methods to maintain this vital part of the global economy.

[1] CNBV (29 April, 2020) https://www.gob.mx/cnbv/articulos/criterios-contables-especiales?idiom=es

© Alliance for Financial Inclusion 2009-2024