About

About

Online

Online

Data

Data

Forced displacement is one of the most pressing challenges of our time. According to the UNHCR Mid-Year Trends Report for 2023, in July this year the number of forcibly displaced people worldwide was estimated at 110 million. The scale of the crisis is impeding progress towards achieving UN Sustainable Development Goals (SDGs) as well as commitments to “leave no one behind.” The protracted and complex nature of forced displacement requires that urgent life-saving humanitarian support be complemented by development action, such as financial inclusion.

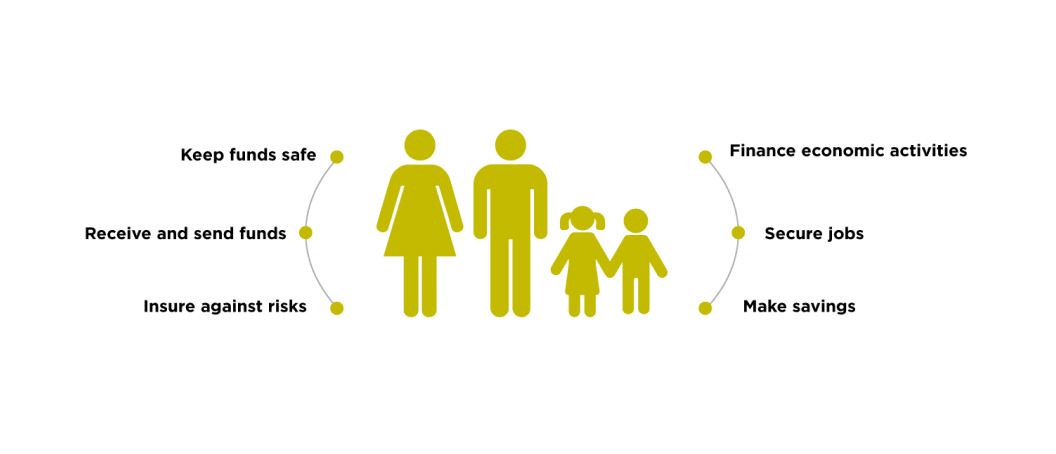

Financial inclusion empowers FDPs to cope under extremely difficult circumstances while also meeting their broader, long-term financial needs. Access to formal financial services creates conditions for FDPs to establish coping mechanisms, build self-reliance and resilience, apply their skills and competencies, restore their livelihoods, realize their full potential, and live with dignity. In turn, they can contribute to the economic growth of their host country, voluntarily return home or resettle in a third country.

Specific challenges in advancing policy and regulation for the financial inclusion of FDPs include:

AFI supports peer-to-peer learning on financial inclusion initiatives that can offer the same opportunities for FDPs as citizens or other country residents, but only when adapted and applied appropriately. Successful programs and best practices indicate that it is necessary to carefully tailor approaches while taking the FDP context into account and adding complementary services where needed.

Financial policymakers and regulators in emerging economies are taking significant steps to adopt innovative policy and regulatory approaches in order to financially include FDPs. In the past year, several AFI members, such as Central Bank of Mauritania, Da Afghanistan Bank and National Bank of Rwanda, implemented policy and regulatory reforms that enhanced access to formal finance for FDPs living within their jurisdictions. This is in addition to efforts by other members, including Bank of Tanzania, Bank of Zambia, Bank of Uganda and Central Bank of Jordan, which have championed this issue for several years now.

Da Afghanistan Bank - Da Afghanistan Bank simplified KYC requirements that allowed FDPs to open transaction accounts at banks, and MNOs with their Ministry of Refugees and Repatriation (MRR) cards, UN Migration card, UNHCR card, and WFP card. The Central Bank also ensured that FDPs are included in Afghanistan’s National Risk Assessment (NRA) and National Financial Inclusion Strategy.

Bangladesh Bank - Bangladesh Bank provided financial services for the Rohingyas by issuing a circular to financial service providers confirming that photo identity documents generated by the Government of Bangladesh, and UN organizations are acceptable for KYC purposes.

Bank of Zambia - Bank of Zambia granted approval for mobile money service providers to provide MFS (within transaction and balance limits for mobile money and e-money) to refugees who present identification cards or registration documents issued by the Ministry of Home Affairs. These mobile money service providers include Airtel Money, Zoona, Kazan, Zamtel Kwacha, and MTN Mobile Money.

Bank of Tanzania - Bank of Tanzania worked closely with the Government of Tanzania and Financial Intelligence Unit (FIU) on the National Risk Assessment (NRA) to identify risks that can be posed by refugees in the financial system. Establishing the level of risks is important to develop tiered KYC processes and integrate into the second National Financial Inclusion Framework (NFIF 2.0). Bank of Tanzania continuously empowers banks and MNOs to develop products that are suitable for FDPs.

National Bank of Rwanda - National Bank of Rwanda enabled digital cash transfer programs for refugees in Nyabiheke, Gihembe, and Kigeme camps to complement other humanitarian efforts. The Bank work with partners in visiting refugee camps to raise awareness on financial consumer protection regulations, and encourage adoption of cashless means of payment.

Central Bank of Jordan - Central Bank of Jordan included refugees in the Jordanian National Financial Inclusion Strategy (2018-2020). The Central Bank also launched the Jordan Mobile Payments (JoMoPay), its national centralized payment switch that connects refugees to a payment ecosystem comprising of financial and payment intermediaries such as telcos, banks, and transfer companies. JoMoPay offers benefits to refugees as its KYC requirements are uniquely designed for them to use their UNHCR ID number to register, providing refugees with access to a mobile wallet.

Where appropriate, FDPs should be given the opportunity to indicate their individual preferences and needs. Displaced communities have an important role to play in designing local solutions to advancing financial inclusion.

Evolving payment landscapes and implementation of digital technologies, including biometrics and distributed ledgers, have the potential to substantially improve compliance, cost efficiency, and accountability for financial inclusion of FDPs.

Risk management should address barriers such as compliance with KYC requirements, and FDP issues within the context of NRAs and AML-CFT regulations is a priority. Concerted coordination should continue among financial regulators and policymakers, global and regional standard-setting bodies, UNHCR and other humanitarian agencies, and civil society to develop a clear plan of action.

Financial regulators and policymakers can drive, influence, and facilitate efforts to design and offer formal financial services to FDPs by creating an enabling regulatory environment that fosters innovation yet still ensures sound compliance.

Coordinate with relevant actors to collect data on FDPs and their financial needs

Integrate FDPs into NFIS.

Include FDPs in National Risk Assessments (NRAs) towards implementing simplified CDD for low-risk FDPs

Collaborate closely with key ministries, global and regional standard setting bodies, development and humanitarian agencies, civil society organisations, and the private sector

Improve FSPs’ negative perception of FDPs

Create a regulatory environment to enable FinTech solutions that comply with global standards for financial integrity, stability, and consumer protection.

Adopt digital technologies such as biometrics to substantially improve compliance, cost-efficiency, and accountability for the financial inclusion of FDPs.

Smart policies for Inclusive Green Finance

© Alliance for Financial Inclusion 2009-2024