By Ali Ghiyazuddin Mohammad, Senior Policy Manager, Digital Financial Services, AFI and Oreoluwa Olaitan, MBA Candidate, Asia School of Business

Digital financial services (DFS) have contributed significantly to advancing inclusion, as further evidenced during the COVID-19 pandemic. Given the role of regulations in promoting digital financial services, AFI – through its DFS working group – conducted a study on their state of practice.

By conducting a benchmarking exercise, the DFS state of practice aims to help AFI member institutions identify and address regulatory gaps at country and regional levels. This will also help AFI identify key topics and design services that support member institutions in creating an enabling DFS regulatory ecosystem.

This explainer highlights key findings and analyses from the report. We also compare specific indicators from the DFS regulatory dataset with indicators in the 2021 Global Findex and the present key findings.

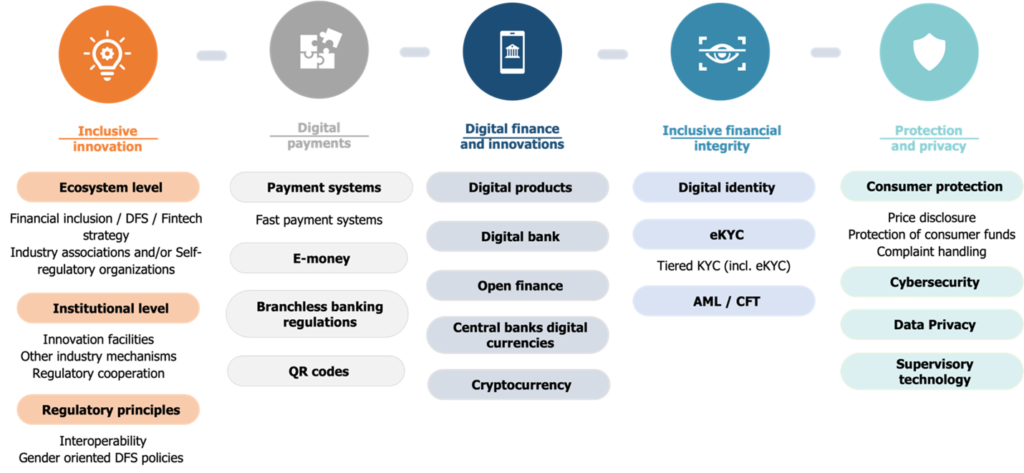

Figure 1:Five DFS pillars & their regulatory indicators

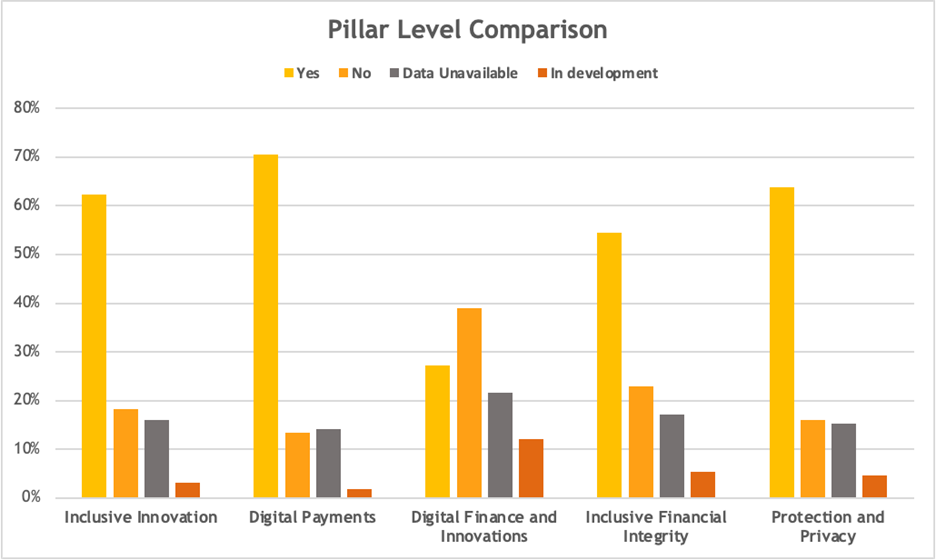

Comparing five DFS pillars and aggregation of their indicators

Implementation of the DFS indicators across the five pillars is shown in the figure below. The second pillar – Digital Payments – has the most policies and regulations implemented, with payment systems act (89%, n = 81) and E-money (88%, n = 81) as its most popular policy areas. On the other hand, the third pillar – Digital Finance and Innovations – which includes open finance, digital banking, central bank digital currencies (CBDCs), digital assets, cryptocurrency etc, has the least number of regulations. Although DFS topics and policy areas are rapidly evolving, regulators seem to be taking a “wait and watch” approach to understand them and their potential impact on the financial services ecosystem.

Figure 2: Pillar level aggregation of DFS Indicators

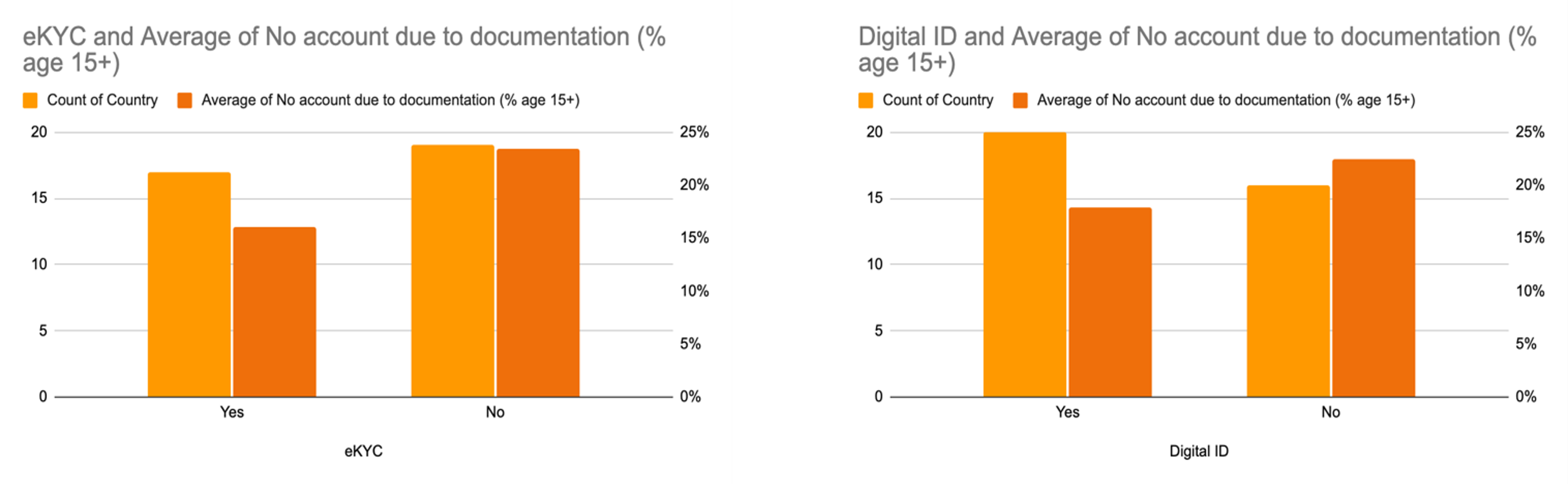

The relationship between e-KYC regulations, digital ID and financial inclusion

Over 40 percent of countries in this study have implemented regulations on Electronic Know Your Customer (eKYC) (46%, n = 81) and Digital ID (digital identity card) (41%, n = 81). Both indicators show a significant association in driving financial inclusion. Simplified KYC and tiered KYC systems ease the documentation requirements for opening financial accounts, hence financial inclusion.

|

Figure 3: e-KYC and average of no account due to documentation (n=36) |

Figure 4: Digital ID and average of no account due to documentation (n=36) |

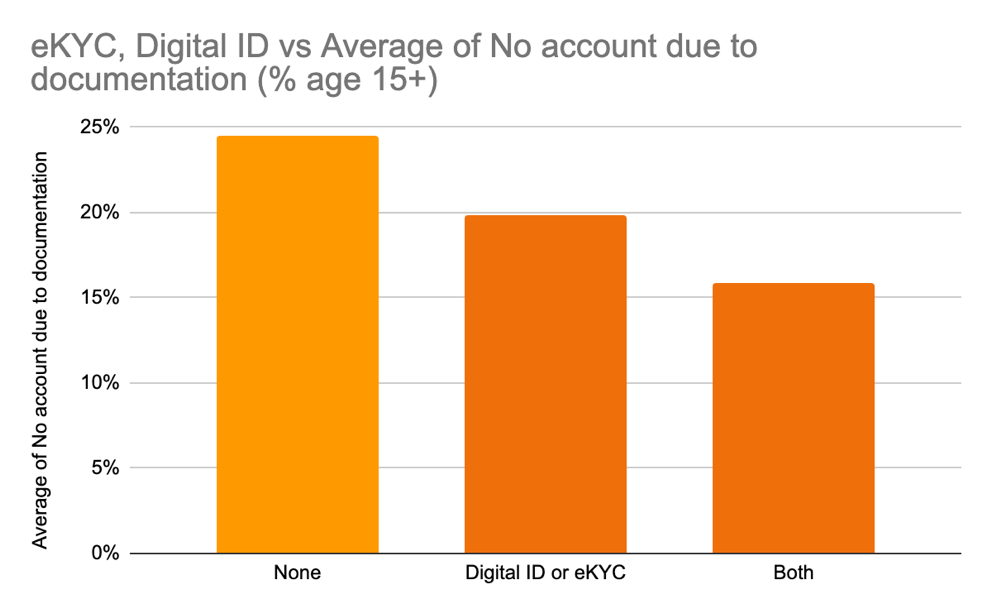

Correlation analysis, with the Global Findex indicator “No financial account due to lack of necessary documentation”, shows that when countries implement e-KYC and digital ID indicators, the two appear to have a compound effect. Countries with both eKYC and Digital ID have fewer people that cite necessary documentation as the reason for financial exclusion, compared to countries with either regulations or none. This shows the need to have eKYC and other regulatory frameworks in place to leverage digital identity and facilitate onboarding of customers and authentication of transactions.

Figure 5: e-KYC, Digital ID and average of no account due to documentation (n=36)

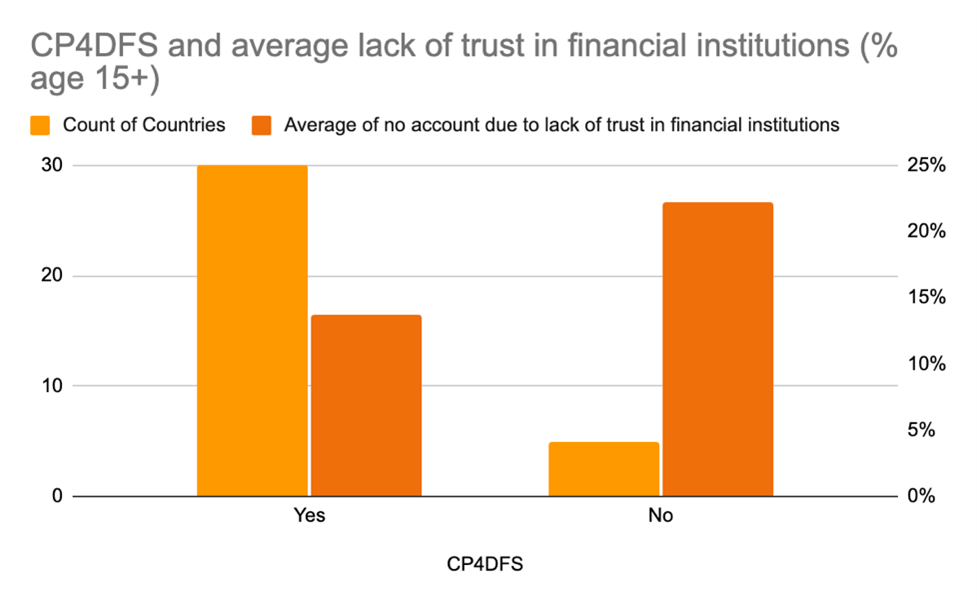

Protection & privacy and financial inclusion

Protection and privacy remain an important regulatory topic, as seen by the number of countries across the network that have implemented regulations from this pillar. Policy areas such as consumer protection, cybersecurity, and data privacy are crucial to mitigating consumers’ DFS risks and strengthening their trust in the financial system.

DFS regulation in consumer protection could be a separate, dedicated set of regulations, or a part of an existing consumer protection framework, but with specific DFS components. In this study, 89 percent of countries have some form of consumer protection regulation in place, but only 57 percent have regulations specific to consumer protection for DFS. Correlation analysis of the “Lack of Trust in Financial Institutions” as a barrier to opening accounts from the Global Findex report (2021), shows that countries with consumer protection regulations specific to DFS report fewer people who are financially excluded, compared to countries that do not.

Figure 6: Protection and Privacy, and average a lack of trust in financial institutions (n=35)

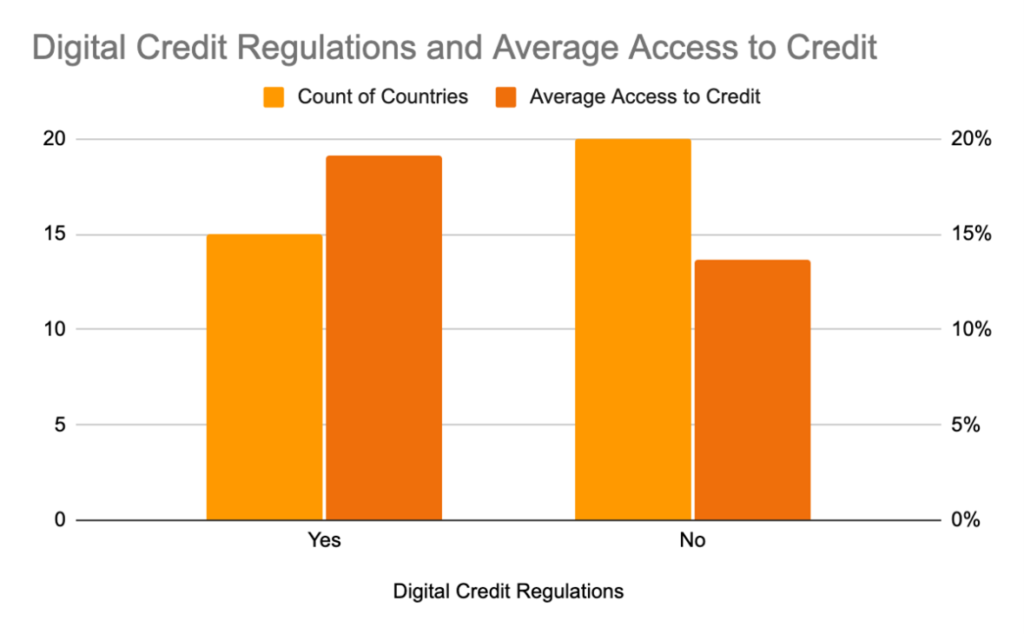

Digital credit regulations and access to credit

Digital credit is another DFS indicator that shows a significant association when compared to indicators from the Global Findex Database. Countries with digital credit regulations average higher access to credit based on the Findex indicator, “Borrowed from any financial institution or mobile money”. These are either separate digital credit regulations or specific digital credit-related guidance in existing credit/lending regulations. While this does indicate causality, we can hypothesize that implementing credit laws/regulations, with specific/separate regulatory requirements on digital lending, provides regulatory clarity and enables more legitimate players to come forward and provide loans to individuals and small businesses. Borrowers also feel safe and confident in availing of loans from licensed, regulated entities.

Figure 7: Digital credit regulations and access to credit (n=35)

While providing insights on the state of DFS regulations across the AFI network and their association with some of the Findex indicators, the study shows a correlation between the variables and does not connote causality. In several instances, there is a time lag between introducing regulatory measures and their impact on the ground. We aim to gather this data periodically to enable time series analysis and a more robust comparison with external data sets. This report is a living document and will continue to change as the DFS ecosystem evolves. as the state of DFS practice changes, we will be including additional indicators to the pillars and to this report.