Special Report Explainer by Laura Ramos (Policy Manager, Inclusive Green Finance), Ghiyazuddin Mohammad (Senior Policy Manager, Digital Financial Services)

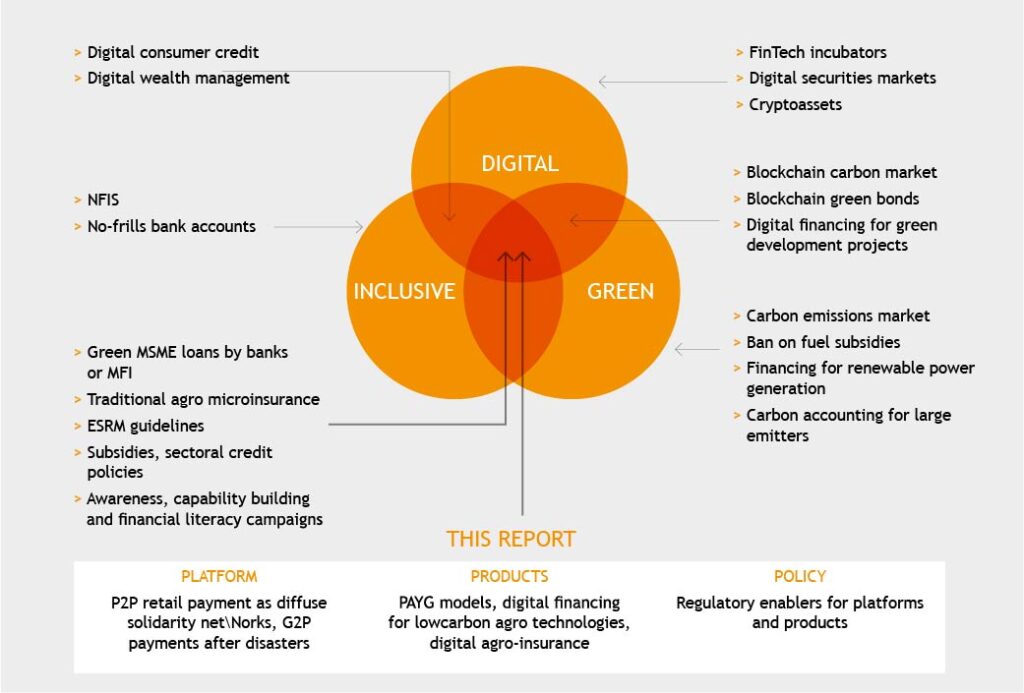

Digital financial inclusion can help leverage finance for climate change adaptation and mitigation, which is why, a joint initiative by AFI’s Inclusive Green Finance Working Group (IGFWG) and the Digital Financial Services Working Group (DFSWG), focused on the overlap between green, inclusive and digital finance in their latest knowledge product “Leveraging Digital Financial Services to advance Inclusive Green Finance Policies” (see Figure below).

This special report showcases how innovative market developments in leading jurisdictions enabled low-income and rural households, as well as micro, small and medium size enterprises (MSMEs), to increase their resilience to environmental risks and adapt to climate change, with digital financial services (DFS) providing solutions to bring about a just transition to a more resilient and environmentally sustainable economy.

Digital channels became an effective tool to rapidly reach vulnerable segments to mitigate negative effects of the Covid-19 pandemic. Regulatory measures such as waivers and incentives for digital payments, information security and business continuity plans, e-KYC frameworks, MSME digitization programs, etc, used during the pandemic carry important lessons in leveraging DFS to respond to climate adaptation and mitigation.

How digital financial services can play a role in contributing to climate adaptation and mitigation?

Analysis on the role of digital finance in advancing inclusive green finance was organized under three key sections: Platforms, products and policy. Joint sub-group between DFS and IGF working groups set for this study gathered insights through interviews with regulators in select jurisdictions, FinTech’s with experience and interest in green finance and through review of available literature.

|

|

Payment Platforms Digital retail payment platforms are the easiest and most effective means for vulnerable populations in developing and emerging countries to manage environmental risks. In many jurisdictions across the developing world, non-bank providers such as mobile network operators or BigTechs have rolled out payment platforms that have turbocharged financial inclusion by enabling digital payments and building a wide network of financial access points. Payment instruments such as emoney or mobile money are increasingly used by low-income and rural households as an informal yet essential risk management device against climate-related economic shocks. Person-to-person (P2P) remittances, especially through digital means, are used to pool and transfer risk among family and community members across distances in ways that are more affordable, trustworthy, and flexible than what most financial firms have to offer. Increasingly, governments add a layer to this digital financial safety net by channeling government to person (G2P) payments via mobile money, emoney or basic savings accounts to those in need, especially after natural disasters. |

|

|

Products Several green digital financial products build on digital retail payment platforms to help households and micro, small and medium enterprises (MSME) adapt to and mitigate environmental risk. Digital savings and loans can help vulnerable parts of the economy become more resilient to shocks and invest in green technologies that turn them from a victim of climate change into a protagonist in the fight against it. Pay-as-you-go solar as a green digital asset financing model deserves special attention because it has beneficial effects not only for financial inclusion and the environment but also for the health and economic conditions of low-income families. Two additional products focus on smallholder farmers, a population particularly exposed to environmental risk. Index agricultural insurance providers can leverage digital technology in order to improve product quality and service delivery for their clients. In recent years, entrepreneurs have developed digital agro platforms that combine access to the market and useful agronomical information with the financial services smallholder farmers demand, all in one cash-free package.

|

|

|

Policy Policy is essential to enable and foster the healthy development of a green inclusive digital financial ecosystem. E-money issuance for non-banks, a risk-based approach to regulation, agent banking, and consumer protection are basic regulatory enablers of inclusive digital finance. The special report outlines the benefits of policy sequencing, where regulators take a modified laissez-faire approach to help the private digital financial ecosystem thrive first and tighten rules subsequently to address market failures. Openness to digital newcomers is not common and requires particular attention by policymakers seeking to foster a green and inclusive digital financial system. Experience with regulatory relief for mobile money in the form of waivers and incentives during the COVID-19 crisis carries important lessons for economic shocks from environmental disasters in the future. Finally, policymakers need to foster the uptake of targeted customer groups such as women and rural households, addressing inequalities in access to digital financial services. |

What are the main recommendations to policymakers to leverage DFS to advance IGF policies?

The insight gathered from the AFI member experiences and expert interviews suggests the following six high-level recommendations:

-

-

- Allow non-banks to establish digital retail payment platforms: policymakers should focus on retail payment platforms that can provide basic but essential services to climate-vulnerable populations.

- Consider policy sequencing: Test and learn, regulatory sandbox and other innovation facilitation approaches, including regulatory policies facilitate market entrance of digital new (non-bank) digital finance providers.

- Lower barriers to entry by adopting a risk-based approach: policymakers should establish tiered KYC and lower identity requirements in line with the results of risk assessment for customers to sign up for mobile money. Regulators should apply a more flexible licensing regime for companies.

- Remove obstacles to private-sector investments in digital financial inclusion for green purposes: policymakers should provide an enabling environment and reduce barriers to market entry.

- Focus on supervisory engagement and outreach, not institutional form: policymakers should keep an open attitude to new (non-bank) digital finance providers and provide collaborations across ministerial and agency siloes.

- Address gaps in access by encouraging uptake among targeted customer groups: policymakers should design capacity building programs and financial literacy campaigns to foster DFS uptake by women, smallholder farmers, low-income households, MSMEs and other sectors.

-